BRACE FOR A 'SWARM-IN' ON THE RINGGIT & THE RUPIAH - CONCERNS GROW RM5 TO THE DOLLAR MAY NOT HOLD - NEITHER CAN 16,500 FOR THE RUPIAH - AMID POLITICAL INSTABILITY IN MALAYSIA, RUNAWAY INFLATION IN INDONESIA

Written by Sam Chee Kong, Politics Now!

KUALA LUMPUR (Politics Now!) - The mood and feelings of despair and desperation currently surrounding the people in Malaysia are reminiscent of the period during the Asian Financial Crisis in 1997.

Besieged by huge debts and balance of payments deficits their economies are vulnerable to a currency attack. In what appeared to be the calm before the storm, the events leading to the eventful moment on July 2nd 1997 caught everyone by surprise due to the speed of the unfolding events.

It started when Thailand unpegged the Baht from the USD. It quickly spread to neighboring countries such as Malaysia, Indonesia and Korea. It set off a series of devaluations which also led to massive

capital flights from the region. Some of those currencies devalued by more than 50% within a

period of few months.

Today, we are revisiting the same scenario again but within a larger context. Meaning we now

have much bigger debts not only confined to Asia but the whole world. It seems we didn’t learn

from our past mistakes.

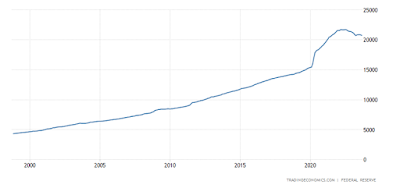

But history tends to repeat itself. What has led to the current crisis? It all started during the Global Financial Crisis in 2008. At that time the world is threatened with a global recession if something is not done. The catalyst for the GFC was due to the bust of the US housing market. Housing prices are collapsing and borrowers unable to repay their mortgages. To illustrate the problem, the following is the 25 year interest rate chart of the US.

As can be seen the interest rate back in 2008 was 5.25%. To alleviate the problem or bailout the

economy, it has to be brought down. Thus the Federal Reserve Bank implemented a policy of 10 interest rate cuts which eventually drove it down to 0%. The zero interest rate policy lasted until 2016 when theglobal economy started to recover.

To revive the economy global central banks also began their “money printing” spree. Spurred by the growing economy and optimism, it encouraged banks to give out easy loans to home buyers, credit card, personal and businesses. The following is the money supply M2 chart of the US. Look at the angle of ascent especially during the pandemic years.

Hence to prevent inflation from getting out of hand while encouraging growth interest rates

began to rise as from 2016. However, that came to a halt in 2020 when the world was struck by

the Covid-19 pandemic. Things began to fall apart when countries began implementing

lockdowns. Businesses starting to fail and people are unable to survive on their own not to

mention paying their mortgages, credit cards and personal loans. Moratoriums on payments on

debts are implemented to aid the situation.

This only provided a “band aid” solution as it is only effective in the short term. The elephant in

the room was the huge loans taken by governments and corporations in developing countries

during the early years of post GFC recovery.

Unfortunately most of these loans are denominated in USD. Thus bringing with it one of the most devastating effects of “foreign exchange exposure”. That is exactly how it wiped out many hedge funds by using what known as the “carry trade”. The following best explains how a carry trade works.

https://www.investopedia.com/carry-trade-definition-4682656

Thus , a borrower will be subjected to two major risks. One is the forex exposure or a drop in the

borrower’s currency. Meaning more domestic will be needed to repay the same loan. The

second big risk is the interest rate exposure. Meaning when the interest rate goes up during the

tenure of the loan then the costs of servicing the loans will be higher.

This is exactly what happened to those emerging market economies. And it’s basically a rerun of

the Asian Financial Crisis in 1998. Thus two Asean currencies that I mentioned that risked

collapse is the Malaysian Ringgit and Indonesian Rupiah.

Let’s take a look at some fundamentals of the Malaysian economy.

WORST-PERFORMER RINGGIT

As can be seen USD/MYR is almost hitting the all time low of 4.88 which was recorded earlier in

an intraday spike. Bank Negara Malaysia has intervene in the forex market through buying and

selling the USD to support the Ringgit.

However intervention into the forex market do have it’s unintended consequences if the impact is not sterilize. Such as runaway inflation or the credibility of the government. The main problems during such interventions are mainly in determining the timing and the amount of intervention. This presents a huge dilemma to most central banks as both involves research and understanding in both technical and fundamentals of the country.

This is also a highly complex maneuver as we are dealing with an ever changing real time situation. Thus in most cases a corrective intervention has to be taken immediately after the first attempt. To put it into perspective, if you were to look into “the hedge book” of a corporate treasurer, within a single month you can see multiples {up to 10} call or put options executed following an initial trade so as to cover the errors of forecasting.

From what I see from the chart, I reckon Bank Negara Malaysia (BNM) has failed to performed

it’s task of stabilizing prices. Our Ringgit has been on the downward spiral despite repeated

intervention and it is almost at the all time low. This has caused spikes in prices in most food and

consumable items as many of them are imported such as rice, vegetables, wheat and so on.

And despite the weakening of the Ringgit, it is a miracle that our inflation rate is still maintained

at 2%. This I called a bluff. I have written a report on how our Government manipulated our CPI

(Consumer Price Index) basket of goods so as to provide a miniscule rate of inflation. Here is the

report which was published in www.MarketOracle.co.uk. I suggest you read the article in order

to fully understand how a country’s CPI calculated behind the scene. (https://www.marketoracle.co.uk/Article35613.html )

As can be seen from the report the CPI figure is being manipulated through bias in grouping,

weighting, under reporting and so on. Thus I can conclude that Bank Negara has failed in it’s

mission in maintaining price stability.

The following is the chart of our inflation rate.

So, do you all believe our inflation rate is still at 2%?

Despite our Ringgit plunging to a new low, our exports surprisingly does not tag along. Meaning

when Ringgit fall our export products will be cheaper than our competitors. But it is not

happening. Below is our export chart.

From the forex chart above you can clearly see that our Ringgit starts plunging last year. As

previously mentioned cheaper Ringgit equates cheaper Malaysian goods and thus will increase

demand for our products. But when you look at our export chart above, it is not happening. In

fact it reverses or went down. What happened? Is this a new conundrum in the economics

space? Lower exchange rate = lower exports?

MALAYSIA NO LONGER COMPETITIVE, RM5 TO THE US$1 MAY NOT HOLD

What I can determine is that our products are no longer competitive. Even though or Ringgit fas

fallen substantially, it is not enough to compensate for the increased costs of production

incurred by our manufacturers.

One simple reason most of our industries are still labour intensive. We needed to bring in huge number of foreign workers because locals reckon those

jobs are only good for foreigners. Thus they prefer jobs in the gig economy such as delivery boys

for online platforms such as Grab or FoodPanda.

RINGGIT HORSE HAS FLED THE BARN

The second and more ominous reason is we are lagging behind our neighbors such as Thailand and Singapore in applying industrial automation such as robotics. (https://nixma.com/why-asean-is-leading-the-industrial-robotics-adoption-race/ ).

Our once mighty rubber glove industry is currently being decimated by international

competitors such as Thailand and China. During the pandemic years our rubber glove companies

are raking in RM billions in profit. However this led to the rush in rubber glove production from

China and Thailand. As a result there is a supply glut which lasted years already. Hence the price

plunged back to pre pandemic level (https://theedgemalaysia.com/node/685359 ).

Our glove manufacturers still depended on Bangladesh, Nepal, Vietnam, India, Cambodia,

Indonesia and you name it for our supply of workers. While our competitors in China and

Thailand are applying more automation into their production. In China, they have already

automated their rubber tapping. (https://blog.st.com/rubber-tapping-robot )

Hence, coming back to our discussion on foreign exchange, what I read the other day was that an

official from BNM claimed that they have yet to intervene into the forex market. They have the

necessary tools to reverse our Ringgit weakness. I am just wondering what secret tools they

have in mind? Hiking rates? Direct intervention into the forex market? Open market opeations?

Issuing Ringgit denominated securities to attract foreign capital inflows?

As for the Ringgit, I reckon the horse has left the barn. Whatever they do next might be “too

little too late”. In any aspect I am not surprised to see the Ringgit breaking the 5.00 level before

December 31st 2023.

Reasons being it is futile to go against the trend. When our Government’s credibility is at stake due to political instability like now. It is very easy being a victim to those currency vultures. I got a feeling they are now encircling the Ringgit waiting for the plunge once the Ringgit breaks 5.00. After that it will be no surprise Ringgit to test the 5.50 level next year as round figures such as 5.00, 5.50 or 6.00 tends to be the strongest points.

BRINGING THE BAZOOKA TO THE INTERST RATES GUN FIGHT

As for the Indonesian Rupiah, I reckon there has been much intervention of multiple methods

and size of commitment. Bank Indonesia has been actively intervening the Rupiah since last year

to prevent it from going above the 16,000 level against the USD. What I can say is that the

16,000 level is very important for the Indonesian policy makers. Because Indonesia depended a

lot on their imports for their local industries especially industrial, electrical, electronic parts,

food such as wheat for their instant noodles and so on.

Thus it can be said the 16,000 level is the threshold of the currency as anything above that will cause devastating effect to their economy. Today it closed at 15.935.00. Just a tad from 16,000.

It is said that many local SMEs are refraining from increasing their prices afraid of losing

customers. As a result they are absorbing the increased costs due to weakening Rupiah. Bank

Indonesia has tried direct intervention, open market operations, selling tradable Rupiah

denominated securities hoping to attract capital inflows so as to not depend on using it’s

depleting foreign exchange reserves to defend the Rupiah.

To further add substance to the effort, Bank Indonesia brought out their bazooka to the gun fight. Unfortunately even though they hiked their interest rate by another 25 basis points, it failed to prevent further deterioration of the Rupiah.

Despite the weakness of the Rupiah, exports did not increase but in fact decreased. As shown

below.

I reckon it is another case of un-competitiveness as in Malaysia. It failed to lure in buyers as the

depreciation of Rupiah is not enough to cover their high costs of production. This is a serious

issue and need to be address fast if not it will risked widening the development gap further. Take a look at the Balance of Trade.

COMPLEX & DEEPLY-ROOTED PROBLEMS

It seems that Indonesia has more complex and deep rooted problems. As can be seen from

above their Balance of Trade is declining since the reopening of most global economies since

2022. When Balance of Trade (Exports – Imports) declines, it indicates either the country is

losing competitiveness or imports costs surging due to weakening Rupiah or both.

From what I see, it’s both as exports also falters during their economic recovery. Moreover, I reckon Bank Indonesia is running out of tools as they have been aggressively intervening in the forex market.

This can be shown by their huge depletion of foreign exchange reserves in recent months.

Since March their foreign exchange reserves has been depleted by more than USD 10 billion.

Thus I reckon it will again futile to employ such tactic in future to support the Rupiah. Another

intriguing aspect about the Indonesian economy is a sudden explosion in their M1 money supply

in late December 2021. The M1 money supply more than doubled hinting huge money printing

by the Indonesian government. Take a look.

Thus I have some reservation regarding their low inflation rate which happens to be 2.56%.

Take a look at the inflation rate chart.

How can Bank Indonesia manage to bring down inflation by more than 50% since the beginning

of the year when the Rupiah is weakening and import costs rising?

Apart from that, the Rupiah seems to have a direct relationship with their stock market. Whenever the Rupiah nears the 16,000 level it crashes. For example as for today the Rupiah rebounded to 15,935 from yesterday’s 15,884. The Jakarta Composite Index plunged 109 points or 1.63% to 6642.41. A loss

of about 600 points from the high.

Moreover the JCI is heavily supported during the pandemic years using unorthodox measures.

For stocks valued between Rp 50 and Rp 200, their limit down is 7% while limit up is 35%. Stocks

at Rp 201 to Rp 5000 limit up 25% and down 7%. While those above Rp 5000 limit up is 20%.

This clearly sets up for a bullish sentiment. Thus this helped powered Indonesian stocks to a new

record high of 7235.

In summary, I reckon this is a very risky strategy as without Government support, the stock market

will not be able to stand on it’s own. Further to this it is expected that Indonesian corporate

earnings is going to take a hit as costs of production went up due to importation costs.

A lot of SMEs will have to raise price to survive. By doing this it will help raise the inflation rate

throughout the country. Further to this with the strengthening of the dollar, it will have serious

repercussions on the Indonesian economy because Oil & Gas is Indonesia’s number one

import. With both items priced in dollars, it is going to have an effect on the costs of

production, transportation and so on.

POLITICAL INSTABILITY IN MALAYSIA, RUNAWAY INFLATION IN INDONESIA

In summary, what I can foresee is that both the Ringgit and Rupiah are facing an ominous

situation in the coming months. Malaysia with it’s political instability and Indonesia risking a

runaway inflation will have an uphill task to defend their currencies.

Despite numerous strategies and interest rate hike, it doesn’t seem to be working. Both currencies are at their all time lows coupled with depleting foreign exchange reserves, options are limited. And this

presents an excellent opportunity for currency traders to do a “swarm in” collective effort to

drop those currencies.

In a nutshell, I am not surprise to see Ringgit touching 5.00 and Rupiah 16,500 by December 31 st 2023. If these levels are breached new contingency plans are needed. I hope capital controls happening will not be enacted. But more unorthodox economic measures needed turn this tide. Unfortunatelt, time is not on their side as timing is everything in the markets.

Written by Sam Chee Kong, Politics Now!

Politics Now!

Comments